Smartphone shipments from original design manufacturers/independent design houses (ODMs/IDHs) declined by 5% year-on-year (YoY) in 2022, according to Counterpoint Technology Market Research’s latest Global Smartphone ODM Tracker and Report.

According to Senior Research Analyst Shenghao Bai, the YoY decline in ODM/IDH companies’ shipments in 2022 was driven by weak performance from OPPO Group, Transsion Group, Lenovo Group and HONOR.

“These smartphone OEMs were hurt by economic headwinds during the year and the negative effects were passed directly to their ODM partners,” said Bai. “However, the contribution of ODMs toward smartphone shipments has been increasing. For instance, the proportion of ODM shipments in vivo rose rapidly in 2022 after the brand kicked off its cooperation with Huaqin and Longcheer.”

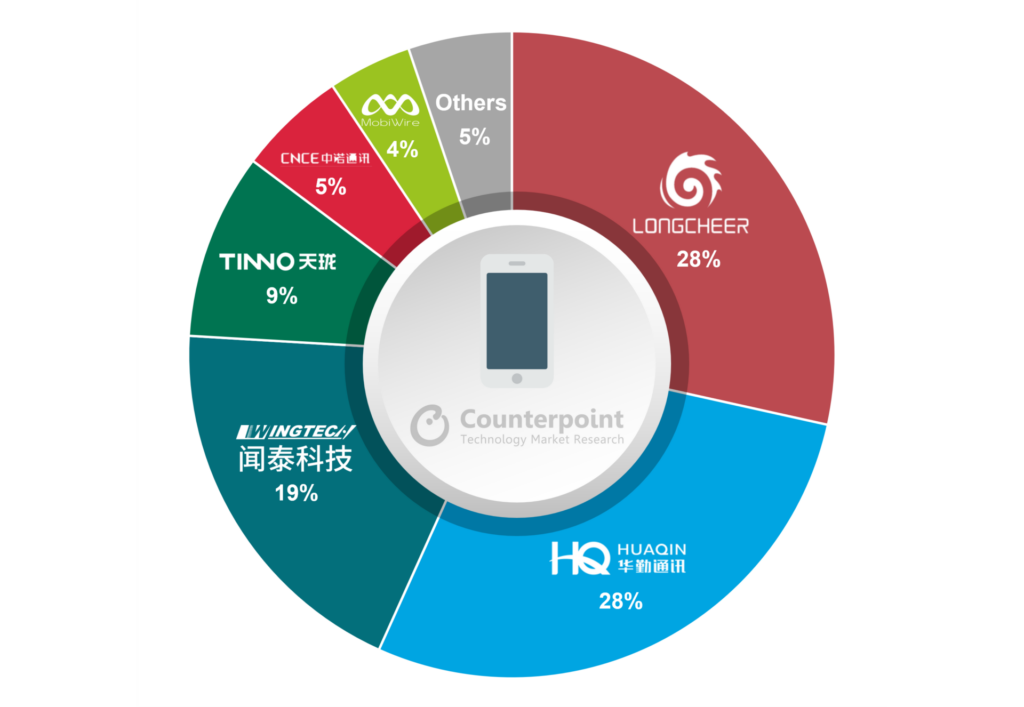

Longcheer, Huaqin and Wingtech continued to dominate the competitive landscape of the global smartphone ODM/IDH industry in 2022. The companies, also known as the ‘Big Three’, accounted for 76% of the global ODM/IDH smartphone market in 2022 compared with 70% in 2021.

Global Smartphone ODM/IDH Vendors Shipment Share, 2022

Source: Counterpoint Research’s Global Smartphone ODM/IDH Tracker, 2022

“Longcheer’s shipments surged in 2022 due to strong orders from Xiaomi and Samsung, helping the company rank first in terms of shipment share. Meanwhile, Huaqin managed to remain one of the leaders among ODMs due to its diversified client portfolio and an increase in orders from vivo, the top smartphone OEM in China. In contrast, Wingtech saw only a modest YoY increase in shipments, as it continues to view smartphone ODMs as only one component of its overall ODM business,” Senior Research Analyst Ivan Lam said. “In Tier 2, Tinno’s shipments continued to grow steadily after the spin-off of the WIKO brand, due to successful marketing with major carriers in the US, Japan and Africa. Its partnerships with Lenovo and Transsion also contributed to an increase in shipments. MobiWire experienced a significant rise in shipments after winning Transsion’s projects. Additionally, its recent collaboration with TCL is expected to serve as an alternative revenue source as TCL shifts its focus to the below $300 segment.”

“The leading ODM players are actively expanding their ODM and EMS services to other smart device categories, with Huaqin ranking first in shipments in broader smart devices categories. To enrich their portfolios, ODMs are actively exploring sectors such as components, semiconductors, automotive and XR products. They are trying to put more helmsmen in place to ensure their company sails more steadily in the face of global headwinds,” Lam said.

China’s manufacturing sector has been recovering after COVID-19 restrictions in the country were lifted. China’s capacity is expected to return to normal by 2023. Meanwhile, the global electronic industry’s manufacturing diversification continues to grow.

Bai said, “Smartphone OEMs are investing heavily in India. Meanwhile, EMS companies are expanding their assembly lines to India, Southeast Asia, LATAM and other regions. India’s local manufacturing will be able to fulfill the domestic demand and will also be sufficient for exports.”

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

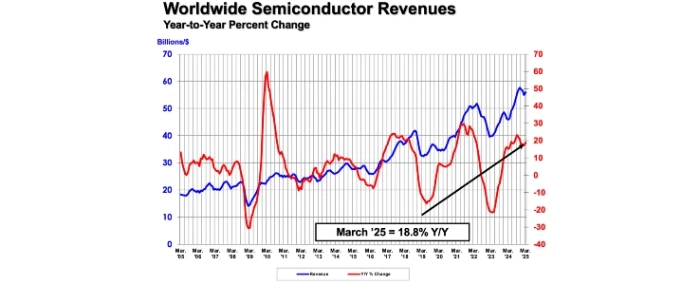

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last