The oversupply of semiconductors is continuing for a long time. In addition to consumer-oriented electronics such as smartphones and personal computers, data center investments by IT giants are slowing down. Demand, centered on cutting-edge semiconductors, is declining. It is expected that the balance between supply and demand will not be achieved until after the fall of 2023. However, demand for semiconductors in fields such as pure electric vehicles (EVs), where demand is growing, continues to outstrip supply, and supply constraints persist.

Due to the sharp decline in demand for smartphones and other effects, memory for data storage, etc. has rapidly turned into excess supply since the second half of 2022. Semiconductors for smartphones and personal computers turn to oversupply as of July to September 2022. Despite the gradual progress in the suppression of semiconductor supply and inventory digestion, the restoration of the balance of supply and demand for semiconductors for smartphones is expected to wait until October to December 2023, and for semiconductors for personal computers until July to September 2023. IT giants in China and the U.S. are reducing investment due to slowing advertising revenues and other impacts, and demand for data center-oriented semiconductors is slowing. It is expected to tend to oversupply by January to March 2023.

In contrast, demand for automotive and industrial-oriented semiconductors continues to outstrip supply. Although the number of parts available with shorter lead times is increasing, CoreStaff, a semiconductor trading company, said, "If one type of semiconductor and electronic parts cannot be procured, they cannot be produced, and other parts have to be turned into inventory. Centering on the semiconductor parts with old production technology, it is still difficult to procure sufficient quantities.

Especially for automotive semiconductors, the supply shortage is expected to be maintained in 2023. In addition to automakers regaining production, the increase in semiconductor usage per vehicle is also pushing up demand. Against the backdrop of increasing demand for automotive semiconductors, power semiconductors for current control and analog semiconductors for power management, etc. are "less investment in equipment, and it may be difficult to increase supply rapidly. Both will maintain a shortage of supply in 2023.

Toyota and Honda were affected by the shortage of semiconductors, and production in December was lower than previously planned, while some plants, including domestic plants, will adjust their operating rates in January 2023.

Thanks to the support of national and regional governments, new plants of Intel and TSMC will come into operation in 2024 in the United States. Micron Technology and others have also announced large-scale investment plans. While betting on long-term demand growth is indispensable for investment, capacity will increase rapidly. If capacity increases faster than demand recovers, there is a risk of further oversupply centered on cutting-edge products.

source:Japan News

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

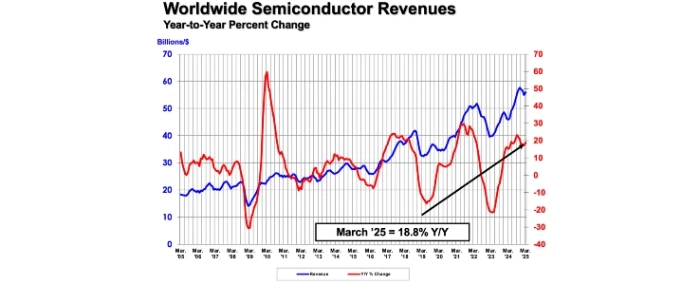

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last