Research institute TrendForce recently predicted that with the release of new production capacity of TI, the global power management chip production capacity will increase by 4.7% in the first half of 2023, while demand is still affected by the off-season preparation, consumer electronics demand is weak and other factors, most segments will continue to bring down the price pressure, is expected to continue to drop 5-10% in the first half of the offer, while the performance of automotive products will remain Stable.

The agency further analyzed that the current power management chip market IDM still dominates the global shipment market size, IDM industry combined market share of 63%, of which TI and accounted for 22% market share to become the leading manufacturers. In 2022, IDM manufacturers due to the impact of inflation and price increases, further boosting ASP, but Fabless manufacturers have been the first to show weakness.

TrendForce said that the power management chips used in products including notebooks, tablets, TVs, smartphones, etc. have started to drop in price since the third quarter of 2022, with a quarterly decline of 3-10%, and demand in the network communications and industrial sectors has also loosened by the fourth quarter. At present, only a few industrial (defense) and automotive demand remains stable, orders are scheduled until the second quarter of 2023, the pressure to reduce prices is not great, but because of this type of high-end products more than 83% of the market in the hands of large IDM manufacturers, Fabless manufacturers are trying to cut into the product sample testing in the ongoing.

According to the agency's survey, the current average delivery time of power management chip Fabless manufacturers for 12 to 28 weeks, and even some models of products such as panel power management chip because of the inventory backlog, as long as the order can be shipped immediately; and IDM large manufacturers are still generally longer delivery time, non-vehicle delivery time of 20 to 40 weeks, while the vehicle delivery time is more than 32 weeks, there are also a few manufacturing, assembly and inspection process is more cumbersome products are still in the state of allocation.

source:aijiwei

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

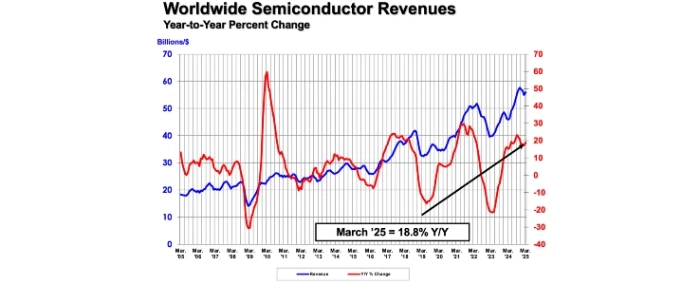

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last