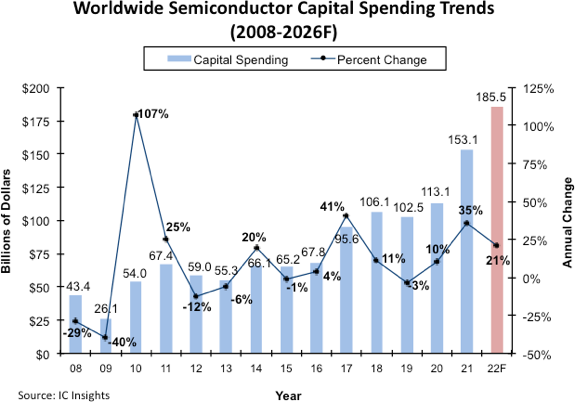

According to the latest data released by IC Insights, a leading semiconductor analyst firm, shows that the three years from 2020-2022 will be the first three-year period since 1993-1995 when capital expenditures achieved double-digit growth.

IC Insights adjusted its 2022 global semiconductor capital expenditure forecast, which now shows a 21 percent increase this year to $185.5 billion, as follows:

This is a decrease from the $190.4 billion and 24% growth forecast earlier this year. Despite the downward revision, the revised capex forecast still represents a new high level of spending.

Utilization rates remain well above 90% for many IDM plants and 100% for many pure-play foundries in the first half of the year, as the economic recovery during the epidemic kept orders strong.

Semiconductor capital spending is now expected to reach $338.6 billion for the two years combined in 2021 and 2022. IDMs and foundries are investing heavily in expansions for the manufacture of logic and storage devices using leading-edge process technologies. However, strong demand and continued shortages of many other important chips, such as power semiconductors, analog ICs and various MCUs, have led suppliers to increase manufacturing capacity for these products as well.

Despite all of this positive news, soaring inflation and a rapidly slowing global economy caused semiconductor manufacturers to reassess their aggressive expansion plans mid-year. Several (but not all) suppliers, particularly many of the leading DRAM and flash memory manufacturers, have already announced cuts to their capital expenditure budgets for the year. More suppliers are noting that they expect to cut capex in 2023 if they assess capacity needs based on the industry absorbing three years of strong spending and slowing economic growth.

source:aijiwei

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

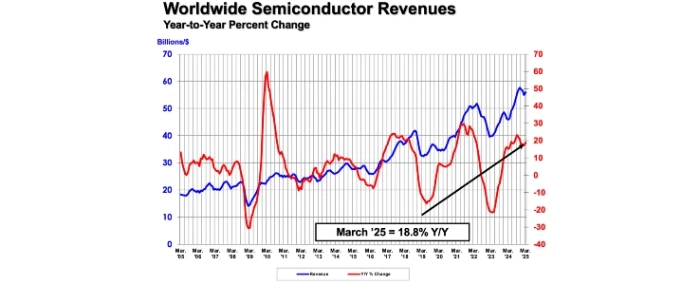

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last