Since 2022, the consumer market, as an important driving force of the global semiconductor industry, has been affected by the war, the epidemic and inflation, and the terminal market demand is sluggish, the power of manufacturers to stock up is down, and the inventory level of consumer products has generally increased.In the first quarter of 2022, the proportion of consumer products in the operating revenue of global wafer manufacturers declined.Among them, the proportion of smartphones in TSMC's operating revenue fell to 40%, down about 5 percentage points year-on-year, and consumer electronics also fell to 26% and 52%, respectively, down about 1 percentage point and 4 percentage points year-on-year, respectively.

CINNO Research statistics show that in the first quarter of 2022, the average inventory turnover days of Chinese IC designers increased to 192 days, an increase of about 58 days from the first quarter of 2021.For SMIC, Huahong and other manufacturers, which account for a relatively high proportion of domestic customers, the rising inventory level of domestic IC design manufacturers brings certain variables to their future revenue growth point.

At present, the upstream price of semiconductor to the downstream transfer is blocked, IC in the demand and price is more obvious differentiation.Among:

· CINNO Research data shows that in the first quarter of 2022, the average inventory turnover days of domestic consumer IC design companies increased to 201 days, and the market demand weakened significantly; while the average inventory turnover days of domestic simulated IC designers increased to 135 days, less than the average inventory turnover days of domestic IC designers.

· At present, the semiconductor market has undergone structural differentiation, and automobiles and some HPC and A loT chips still have significant market growth momentum, but the supply and demand relationship between electronics consumption, PC, NB and other markets have changed.

· The analog chip market has the characteristics of long life cycle, wide downstream application and anti-cycle. At the same time, the improvement of the penetration rate of new energy vehicles brings sustainable development momentum to the analog chip market.

At present, although the global semiconductor industry is facing many challenges, such as inventory adjustment, structural capacity shortage, and weakened terminal demand, but the new infrastructure, dual-carbon, Internet of things, new energy and other market power is still good.From the perspective of wafer manufacturing, the global foundry wafer market will remain strong in 2022, and with the continuous optimization of the product portfolio, the confidence of the global semiconductor industry will not decrease.

Source:国际电子商情

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

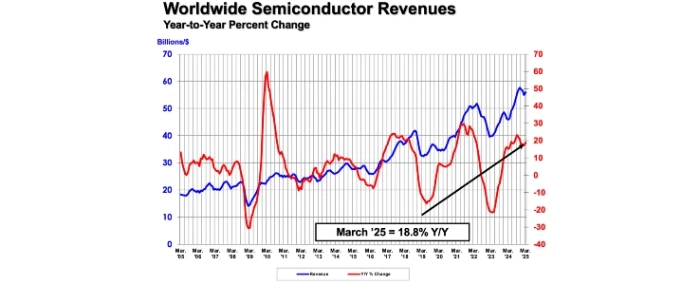

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last