Chinese foundries have experienced a faster recovery in capacity utilisation compared to their peers, says TrendForce, thanks to trends like IC domestic substitution and policies like “China for China”.

Chinese foundries have experienced a faster recovery in capacity utilisation compared to their peers, says TrendForce, thanks to trends like IC domestic substitution and policies like “China for China”.

Some processes are already operating at full capacity and the traditional H2 peak stocking season —combined with delays in expansion due to export controls on US equipment—may extend capacity tightness until the end of the year.

This situation might lead to price increases for specific processes, which is a shift from the previous low-price competition strategy aimed at volume.

Taiwanese foundries are benefiting from increased orders due to out of China demand, leading to better-than-expected capacity utilisation rates for PSMC and Vanguard in H2.

However, overall demand for mature processes remains weak, with average capacity utilisation still around 70–80%—indicating no significant shortages.

Only TSMC is seeing full capacity utilisation in its 5/4nm and 3nm nodes due to strong demand from AI applications, new PC platforms, HPC applications, and high-end smartphones.

Its capacity utilisation is expected to exceed 100% in the second half of the year, with visibility extending into 2025.

Given cost pressures from overseas expansion and rising electricity prices, TSMC plans to raise prices for its advanced processes, which are experiencing strong demand

A significant amount of new capacity is expected to come online in 2025, says TrendForce, including TSMC JASM, PSMC P5, SMIC’s new Beijing/Shanghai plants, HHGrace Fab9, HLMC Fab10, and Nexchip N1A3.

This increase in mature process capacity could intensify competition and impact future pricing negotiations

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

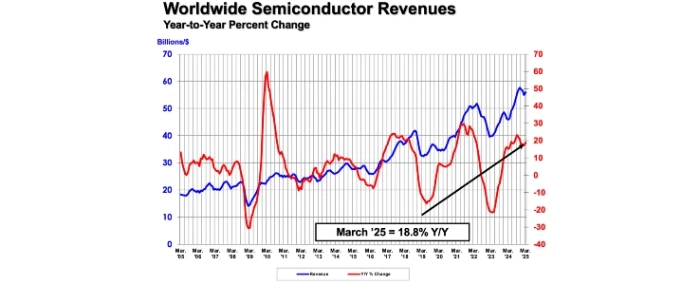

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last