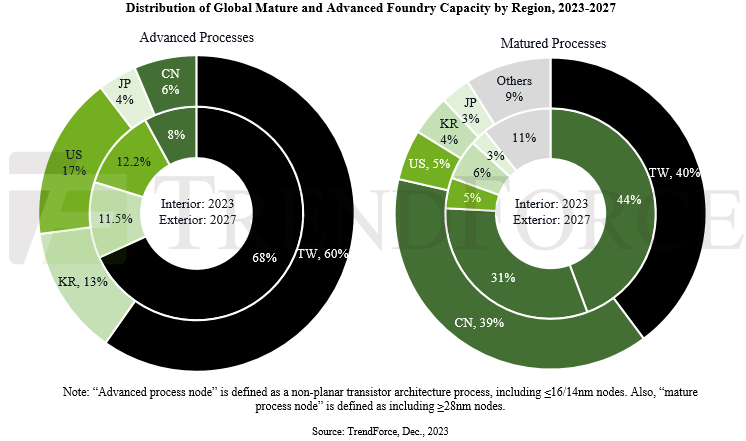

The share of the foundry industry now held by Taiwan and Korea will shrinkto 41% and 10% respectively by 2027, says TrendForce.

Currently Taiwan holds approximately 46% of global semiconductor foundry capacity, followed by China (26%), South Korea (12%), the US (6%), and Japan (2%).

In advanced manufacturing processes (including 16/14nm and more advanced technologies), Taiwan leads with a 68% global capacity share in 2023, followed by the US (12%), South Korea (11%), and China (8%).

Taiwan holds nearly 80% share when it comes to EUV generation processes (such as 7nm and beyond).

While the US’s share of advanced process capacity is expected to increase to 17% by 2027, TSMC and Samsung will still account for over half of this capacity as they ramp up their US production sites.

China is focusing aggressively on mature process technologies (28nm and older). By 2027, China’s share in mature process capacity is expected to reach 39%, with room for further growth if equipment procurement proceeds smoothly.

As Chinese manufacturers rapidly expand their mature process capacities—backed by government subsidies—this could lead to intense price competition in products like CIS, DDI, PMIC, and power discrete, impacting Taiwan-based foundries like UMC, PSMC, and Vanguard.

Vanguard is expected to be most affected due to its product line including LDDI, SDDI, PMIC, and power discrete. Other companies like UMC and PSMC will maintain their advantages in the 28/22nm OLED DDI and memory sectors.

In response to chip shortages and geopolitical influences, fabless customers are diversifying risk by working with multiple foundries, potentially leading to increased IC costs and concerns over duplicate orders.

Customers are also requiring global validation of production lines, even with long-term foundry partners, to enable flexible capacity adjustments.

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

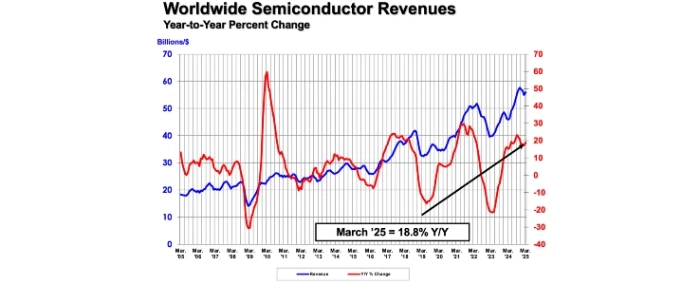

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last