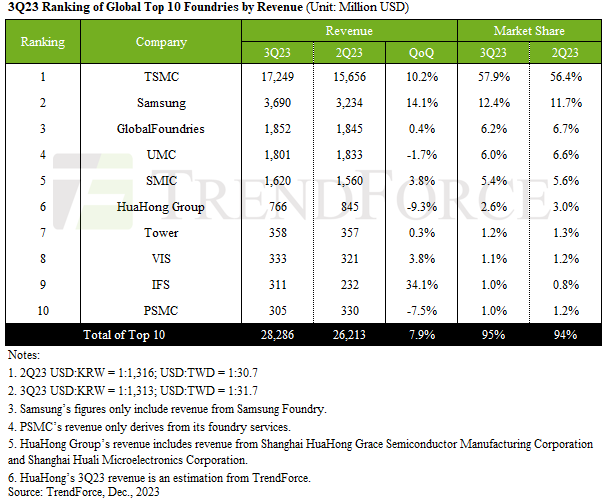

The top ten foundries grew revenues 7.9% to $28.29 billion, and Q4 revenues could grow faster, reports TrendForce.

TSMC, with 58% market share, grew Q3 revenue by 10.2%—reaching $17.25 billion. The 3nm process alone contributed 6% to TSMC’s Q3 revenue, with advanced processes (≤7nm) accounting for nearly 60% of its total revenue.

Samsung grew foundry revenue by 14.1% to $3.69 billion in Q3, driven by orders for Qualcomm’s mid-to-low range 5G AP SoC, 5G modems, and mature 28 nm OLED DDI processes.

GlobalFoundries maintained a stable performance in Q3, with its revenue approximating $1.85 billion, similar to the previous quarter.

UMC’s Q3 revenue declined 1.7% to $1.8 billion. Revenue from its 28/22 nm products saw a near 10% increase, representing 32% of UMC’s total revenue.

SMIC had a 3.8% Q3 revenue increase to $1.62 billion. However, the revenue share from American clients decreased to 12.9%. Conversely, revenue from Chinese clients increased to 84% due to the government’s localisation initiatives and urgent orders for smartphone components.

Notable changes in the rankings from sixth to tenth position include VIS and IFS, with the latter entering the global top ten for the first time since Intel’s financial restructuring.

VIS’ Q3 revenue increased by 3.8% to $333 million—surpassing PSMC to take the eighth position.

IFS had a 34.1% increase in revenue to approximately $311 million.

HuaHong saw a 9.3% decrease in Q3 revenue to about $766 million.

HHGrace maintained steady wafer shipment levels from the previous quarter, but a roughly 10% decrease in ASP led to a decline in revenue.

Tower Semiconductor saw stable demand in the smartphone, automotive, and industrial sectors, maintaining revenue at around $358 million in Q3.

PSMC witnessed a 7.5% drop in revenue to $305 million, with PMIC and Power Discrete revenues declining nearly 10% and 20%, respectively, impacting overall performance.

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

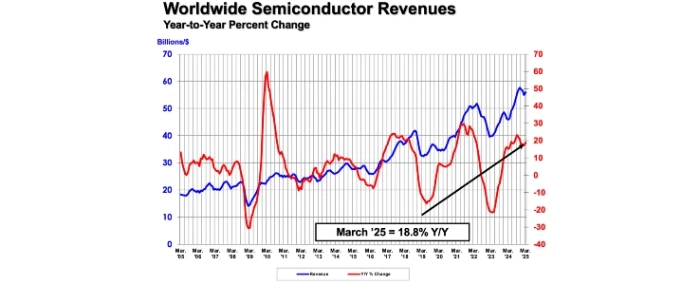

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last