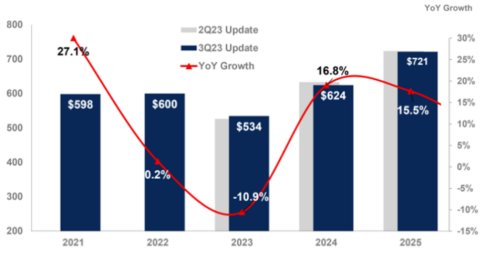

2024 semiconductor sales are projected to grow 16.8% in 2024 to total $624 billion, according to Gartner after a 2023 market which is forecast to decline 10.9% to $534 billion.

“We are at the end of 2023 and strong demand for chips to support artificial intelligence (AI) workloads, such as graphics processing units (GPUs), is not going to be enough to save the semiconductor industry from double-digit decline in 2023,” says Gartner vp Alan Priestley, VP“Reduced demand from smartphones and PC customers coupled with weakness in data center/hyperscaler spending are influencing the decline in revenue this year.”

However, 2024 is forecast to be a bounce-back year where revenue for all chip types will grow (see Figure 1), driven by double-digit growth in the memory market.

Figure 1. Semiconductors Revenue Forecast, Worldwide, 2021-2025 (Billions of U.S. Dollars)

Source: Gartner (December 2023)

The worldwide memory market is forecast to record a 38.8% decline in 2023 and will rebound in 2024 by growing 66.3%.

Anaemic demand and declining pricing due to massive oversupply will lead NAND flash revenue to decline 38.8% and fall to $35.4 billion in revenue in 2023.

Over the next 3-6 months, NAND industry pricing will hit bottom, and conditions will improve for vendors. Gartner analysts forecast a robust recovery in 2024, with revenue growing to $53 billion, up 49.6% year-over-year.

Due to high oversupply level and lack of demand, DRAM vendors are chasing the market price down to reduce inventory.

Through the fourth quarter of 2023, DRAM market’s oversupply will continue which will trigger a pricing rebound. However, the full effect of pricing increases will only be seen in 2024, when DRAM revenue is expected to increase 88% to total $87.4 billion.

Developments in generative AI (GenAI) and large language modelsare driving demand for deployment of high-performance GPU-based servers and accelerator cards in data centers. This is creating a need for workload accelerators to be deployed in data center servers to support both training and inference of AI workloads.

Gartner analysts estimate that by 2027, the integration of AI techniques into data center applications will result in more than 20% of new servers including workload accelerators.

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

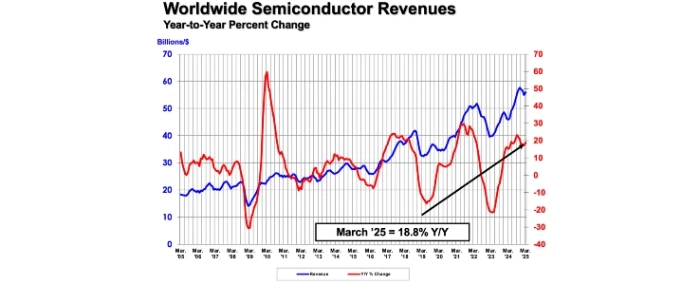

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last