Last year, Aubrey Dunford, the ECSN (Electronic Components Supply Network) market analyst declared the UK electronics components market had returned to normality. At this year’s Electronics Components Forecast, he reclassified its status as a new, new normal.

2024 total forecast 1.6% (min) to 4.1% (max)

At the end of 2022, ECSN suppliers were preparing for 2023 with strong order books and confidence in customer demand and an expectation that prices will generally be maintained. Another prediction for 2023 was that growth in the first half of this year was likely but the second half would be less certain as pent-up demand for 5G and smart vehicle infrastructure systems could bear fruit. The book-to-bill ratio was expected to remain strong in 2023 as lead times returned to more normal levels albeit with some shortages expected. All of this came to pass despite uncertainties such as product availability, global trade and political tensions and falling consumer confidence. At the time, Dunford maintained that authorised distributors are “key to helping the industry find its way through uncertainties”.

Component market sales in 2023 were high with a DTAM of £1886m and a TAM of £4254m, compared to £1722 (DTAM) and £3938m (TAM) in 2022.

For 2024, ECSN members are cautious, based on many statistics. Firstly, inventory is still high, making it difficult to judge demand. Price pressures will be minimal and price levels achieved in 2023 are expected to be maintained. A flat first half is expected, supported by the HM Treasury’s comparison of independent forecasts predicts UK economy average growth of 0.5% for 2023 and 0.4% for 2024. The second half of the year will depend on trade and political tensions, with the added unrest in the Middle East and what effect that will have, not least in terms of oil price rises.

There is still a demand for 5G and vehicle infrastructure systems and some strong demand particularly in the industrial sector as UK manufacturing output rises. There are indications that some market sectors will remain strong, said Dunford, but the overall picture is uncertain. A growth in UK consumption may not be reflected in sales in 2024. It is important to note, said Dunford that manufacturers do not know how much stock is out there, as double ordering of inventory through the pandemic is still to be worked through. The DTAM quarter-on-quarter growth since 2021 is related to price increases in a commodity market rather than increased unit sales, he added.

The one seeming certainty is moderate growth in the first half of 2024, said Dunford, followed by a slight to moderate (~1.4% growth), he estimated.

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

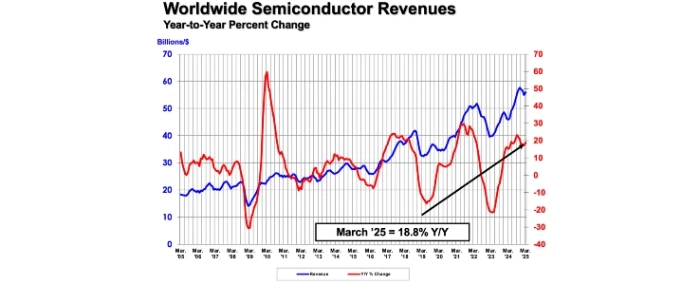

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last