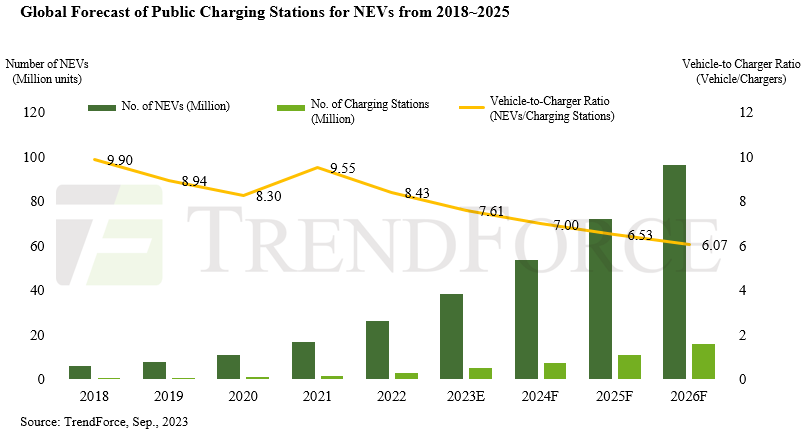

The number of EV charging stations across the world will increase 3x between 2023 and 2026 to 16 million charging points, says TrendForce.

By 2026, the number of EV’s will be 96 billion globally setting the vehicle-to-charger ratio at 6:1, a significant drop from the 10:1 ratio in 2021.

Europe is targeting the construction of 17 million charging stations by 2030.

America, with a little over 200,000 charging stations currently, aspires to hit the 500,000 mark by 2026 which will coincide with a projected EV count of 15 million, delivering a vehicle-to-charger ratio to 32:1.

Around the same period, Europe and China are projected to have ratios of approximately 9:1 and 4:1, respectively.

NEV owners globally grapple with a maze of charging standards. Prominent among these are the US standard CCS1 (Combo), the European standard CCS2 (Combo), Japan’s CHAdeMO, China’s GB/T, and Tesla’s NACS standard. Europe and China offer a simpler scenario for their citizens by adhering to a single domestic standard.

In contrast, the US is a battleground, with both CCS1 and NACS standards vying for dominance. While adapters provide a temporary bridge between the two, the rapid rise of NACS kindles apprehension among CCS1 aficionados about their future stake.

A diverse array of charging standards across the globe means charging equipment manufacturers must adopt flexible product strategies to cater to different market specifications.

GM, Mercedes-Benz, BMW, HONDA, Hyundai-Kia, and Stellantis are joining forces to spin off dedicated charging infrastructure companies.

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

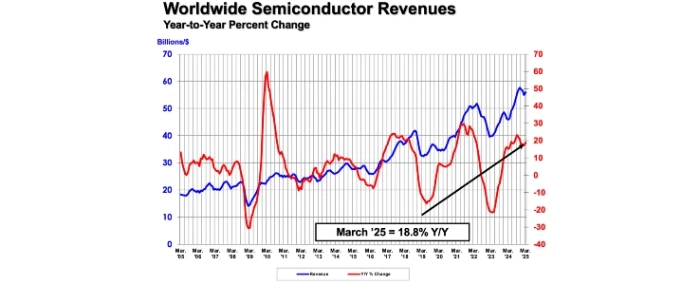

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last