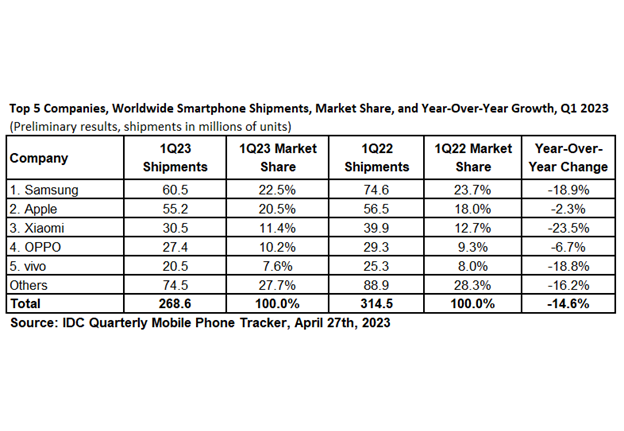

Worldwide smartphone shipments declined 14.6% year over year to 268.6 million units in the first quarter of 2023 (1Q23), according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker. This marks the seventh consecutive quarter of decline as the market continues to struggle with lukewarm demand, inflation, and macro uncertainties. While the decline is more than the 12.7% IDC previously forecasted, the results aren’t surprising. Inventory has remained elevated across regions, however it is in significantly better shape compared to six months ago thanks to reduced shipments and heavy promotional activities.

“The industry is going through a period of inventory clearing and adjustment. Market players remain cautious deploying a conservative approach rather than dumping more stock into channel to chase temporary gains in share. I think is the smart thing to do if we want to avoid an unhealthy situation like 2022,” said Nabila Popal, research director with IDC’s Worldwide Tracker team. “While we are optimistic about recovery by the end of the year, we still have a tough 3-6 months ahead. Everyone is anxious about exactly when the tide will turn and wants to be first to ride the wave of recovery. However, it’s a tricky situation. Anyone who jumps in too soon will drown in excess inventory. Now more than ever, it’s important to keep a close pulse of market. Barring unforeseen elements, IDC expects the market to cross into positive territory in the third quarter and see healthy double-digit growth by the holiday quarter.”

Almost all the regions suffered double digit decline in 1Q23. China witnessed close to 12% drop, which was slightly more than expected despite the recent reopening of the market. Consumers are prioritizing travel and entertainment over smartphone purchases and uncertainty still lingers, which is dampening consumer sentiment. Developed markets like the USA and Western Europe fared better than others with declines of 11.5% and 9.4% respectively. Emerging markets like APeJC, CEE and MEA saw larger 17- 20% declines.

“On a positive note, based on recent discussions we’ve had with OEMs and supply chain it appears the smartphone industry is collectively gaining confidence that we’ll see return to growth late this year, and into 2024,” said Ryan Reith, Group VP with IDC’s Worldwide Tracker team . “The largest supply side pullback in recent months was primarily those brands that serve the mid to low end of the market. This is usually where competition is high, and margins are low. Typically, these players are more hesitant to ramp back up again, and while this may still be the case, we are starting to see signs that optimism is growing amongst this crowd.”

Source: EMS Now

Abonnieren fuer regelmaessige Marktupdates.

Bleiben Sie auf dem neuesten Stand der Branchentrends, indem Sie unseren Newsletter abonnieren. Unser Newsletter ist Ihr Zugang zu erstklassiger Marktexpertise.

ChangXin Memory Technologies (CXMT), China's top DRAM supplier, is reportedly preparing to phase out DDR4 products for server and PC use by mid-2026. As the company pivots to DDR5 and high-bandwid

Japan's push to revive its semiconductor manufacturing is hitting speed bumps as major manufacturers expressed cautiousness over operation or expansion amid weak demand outside of AI.According to

The global semiconductor manufacturing industry entered 2025 with typical seasonal patterns. However, looming tariff threats and evolving supply chain strategies are expected to create atypical season

At the TSMC Technology Symposium 2025 on May 15 in Hsinchu, Taiwan, T.S. Chang, VP of Advanced Technology and Mask Engineering at TSMC, announced the company's accelerated fab expansion plans. Pre

Chinese listed semiconductor equipment and materials companies released their 2024 annual financial reports in late April, revealing strong revenue growth but a decline in overall profitability. Despi

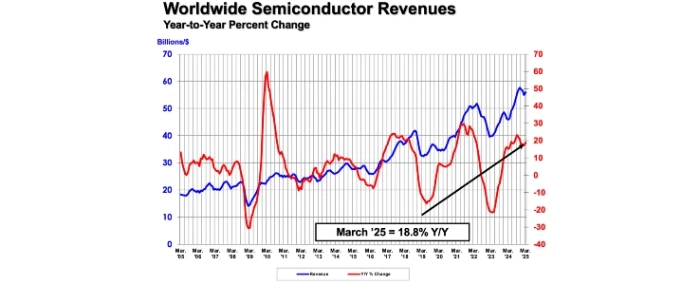

The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached USD 167.7 billion in the first quarter of 2025, marking an 18.8% increase compared to the same period last